In an age of

activist consumerism and investment, and the apparent effects of climate

change, moving towards net zero emissions is the stated goal of many

businesses. The questions is how do we

evolve it from slogan to reality? The

following is taken from “Net Zero or Bust: Beating the Abatement Cost Curve for

Growth”. This article was written

collaboratively by global leaders in the McKinsey Sustainability and

Manufacturing & Supply Chain Practices, including Pauline Blum, Stefan

Helmcke, Ruth Heuss, Thomas Hundertmark, Sebastien Marlier, Dickon Pinner, and

Ken Somers.

Companies can both decarbonise and

boost long-term growth, but it means pushing beyond abatement curves’ focus on

cost and instead empowering people, while making a few big, strategic bets.

Before the COVID-19 pandemic, environmental, social, and governance

(ESG) issues had become priority concerns for governments, businesses, investors,

and consumers. As the world looks forward

to the post-pandemic next normal, these themes are likely to return to the top

of executives’ agendas. Among them, the

need to eliminate emissions of greenhouse gases may be the most difficult to

address. Many companies have already

committed themselves to deep, long-term reductions in greenhouse-gas emissions.

Others will be forced to act by

customers, investors, and governments. Almost

300 large companies have joined the highest tier of the Science Based Targets

initiative, for example — that is, ramping up pressure on suppliers to cut

their own emissions or risk losing business. Business leaders are already telling us that

some of their biggest customers are warning that future contracts will be contingent

on significant emissions reductions.

A growing share of investment capital is also being channeled into

the fight against climate change. Between

2012 and 2018, investment in assets with explicit sustainability goals grew by

15% a year. By 2018, such investments

accounted for 11% of professionally managed assets globally. More broadly, investors are increasingly

concerned about the potential impact of climate-related risks across their

portfolios. In January 2021, BlackRock,

the largest asset manager in the world, asked the CEOs of companies in which it

holds shares to explain how they plan to achieve net-zero emissions by 2050.

And policy makers are piling on further pressure. The European Union, for example, appears

ready to proceed with plans for a cross-border carbon tax, using the proceeds

to fund sustainability initiatives within the bloc. Such policies mean companies are no longer

shielded from environmental legislation by virtue of their location. Any organisation participating in global supply

chains will need to cut its emissions.

Together, these forces mean that decarbonisation is no longer an

option. Across most of the world, companies

with ambitions to stay in business over the long term are already on a 30- or

40-year journey to net-zero emissions.

Like any change journey, the road to net zero involves several

distinct steps. Companies must

understand their current carbon footprints, identify strategies to reduce and

ultimately eliminate carbon emissions, and implement the necessary changes.

These steps would be straightforward, were it not for one catch. Emission-reduction plans tend to be created

using standard “abatement curves,” which take a top-down view and focus on

large-scale technological shifts. These

curves often predict that transition risks, such as falling demand or asset

devaluation or regulatory shifts, will lead to cost increases great enough to

put many organisations out of business long before they reach their net-zero

goals.

In our view, organisations should not let the scale of the

challenge derail their sustainability ambitions. Contrary to what cost curves suggest, big

cuts in emissions can be achieved without large-scale value destruction. What is more, the climate transition will

create historic opportunities for environmentally sustainable businesses to

build new markets, reinvent old categories, and become magnets for top talent. Unilever, for example, says that in 2018, its

Sustainable Living brands grew 69% faster than the rest of its portfolio. And by 2030, the reuse and recycling of

plastics could drive profit-pool growth of US$60 billion for the chemicals

industry, according to McKinsey analysis.

For the journey to become value creating rather than value

destroying, however, companies will need to rethink the conventional approach

to carbon reduction. Moving beyond the

abatement curve involves a combination of top-down and bottom-up activities:

empowering frontline personnel to drive emissions reductions while making

significant long-term strategic bets on markets, technologies, and production

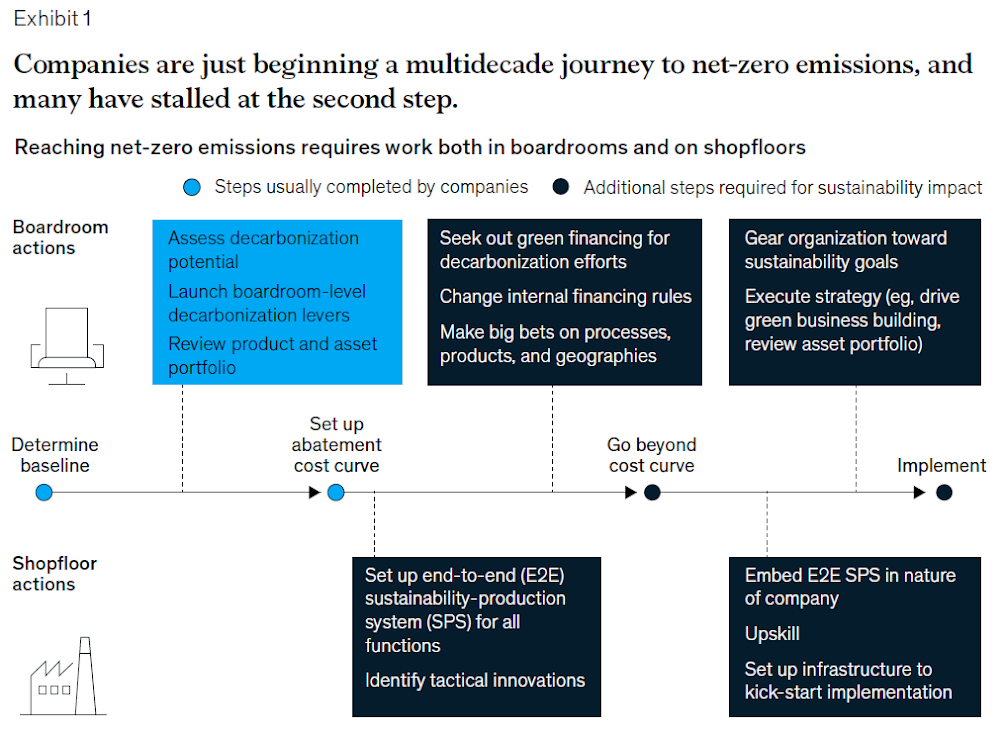

footprint (Exhibit 1).

Even the first step in the carbon-reduction journey — determining

baseline emissions — presents significant complexities. An organisation can use internal data sources,

such as energy bills and procurement records, to calculate its emissions in the

Greenhouse Gas Protocol’s Scope 1 (direct emissions from its own activities)

and Scope 2 (indirect emissions attributable to the organisation’s energy use).

Scope 3 emissions are more difficult to ascertain.

The necessary data are not always available

from suppliers and customers, forcing companies to rely on models or

approximations to build an estimate of their full carbon footprint.

Even a less-than-perfect picture of emissions could still act as a

useful catalyst for improvement. Understanding

the largest sources of greenhouse gas emissions across value chains can help companies

identify quick wins and target energy efficiency improvement efforts. Few organisations make that link, however. Emissions analyses remain locked in the

boardroom, while any improvements made by the front line are simply a byproduct

of efforts to reduce waste and drive up productivity using well-established

lean approaches.

To establish a potential pathway to net zero, companies must

identify the changes that could eliminate emissions from their value chains, then

rank them in ascending order of cost per ton of abated carbon. Today, it is common to map these changes in

the form of abatement curves, which provide the boardroom with a top-down view

of the potential capital investments (often large) in known technologies that

could trim organisation’s emissions.

For business leaders, these abatement curves can be frightening,

especially for industrial companies with energy-intensive processes. Exhibit 2 shows an illustrative

carbon-abatement cost curve for the full value chain of a European automotive

player.

The x-axis of the chart sets out, in ascending order of cost, the

available options for reducing the organisation’s carbon emissions. The y-axis shows today’s cost of each option

per ton of carbon emissions reduced. At

current costs, less than 25% of the path to zero emissions is positive net

present value (NPV).

For this company, the chart’s implications are stark. Eliminating the company’s upstream emissions would

reduce its profits by around €1 billion.

At many organisations, the implications of the carbon-abatement curve

have been daunting enough to stall progress on the deep emissions reductions

that will be necessary over the coming decades. The imperative for today’s leaders is to find ways

to break this deadlock.

Beating the cost curve and building a successful long-term

decarbonisation strategy will depend on big moves in two areas (Exhibit 3). The first operationalises emission-reduction

efforts using known technologies and approaches, moving from theoretical

discussion in the boardroom to pragmatic action in the control room, on the

shopfloor, and throughout the organisation. The second entails big bets on options that

don’t currently appear on the abatement curve, exploring new technical,

strategic, and market opportunities to capture value while reducing

environmental impact.

Translating emissions-reduction goals into a practical reality

involves working on three fronts at once: redefining the decarbonisation

business case in finance, building an integrated sustainability production

system into the organisation, and assembling an infrastructure to support

tactical innovation in operations.

Increasingly, organisations looking to finance emissions-reduction

initiatives can access the necessary capital at low cost. Governments and private investors are showing

a greater willingness to offer long-term loans at favorable terms to fund such

projects. Sustainability-linked bonds

worth more than US$200 billion were issued in 2020, for example, pushing the

total market for such securities above US$1 trillion for the first time. Some programmes even offer borrowing costs

linked to the carbon-reduction impact of investments. In February 2021, drinks maker AB InBev agreed

to a US$10.1 billion credit facility that links interest margins to several

sustainability goals, including group-wide carbon-emissions reductions. Using such structures, companies can often

secure funds for investment at less than half of their existing cost of

capital. That is enough to shift the NPV

of plenty of emissions-reduction projects from negative to positive.

In the context of the transition to net zero, companies can also

revisit their project-investment criteria. At many organisations, projects that improve

efficiency or reduce emissions must today pass the same financial tests as any

other capital investment. That usually

entails a maximum payback period of two years. Extending the maximum payback period to five

years, for example, allows organisations to take a longer-term perspective on investments

that could make a meaningful difference in their climate-change impact.

Alternatively, companies can explore new funding and ownership

models for low-emission assets. Original-equipment

manufacturers or third-party operating companies may be willing to retain ownership

of equipment such as biomass boilers, for example, while the end user pays by

unit of energy consumed. In Romania, for

example, specialty chemicals company Clariant is building a 50,000- ton

capacity plant to produce ethanol from agricultural residues. Steam and electricity for the facility will be

provided by a dedicated biomass cogeneration plant installed and operated by German

energy company GETEC.

Another option for companies is to introduce an internal form of

carbon tax by including the cost of the carbon emissions explicitly as a line

item on the profit and loss accounts of their plants and business units. The funds collected through this mechanism can

then be ring-fenced for use in emission reduction projects. Dutch chemicals company Royal DSM, for

example, introduced such as scheme in 2016, setting an internal carbon price of

€50 per ton.

Many organisations have dozens of potential emission-reduction

projects sitting on their shelves because their business cases failed to meet

the requirements for investment, sometimes by narrow margins. The combination of cheaper, more accessible

capital and a full life-cycle perspective can unlock multiple opportunities to

simultaneously reduce emissions and improve financial performance.

Designing, running, and improving a low-carbon manufacturing

network and supply chain is an intricate task. Organisations will need the skills, processes,

and data to identify and implement efficiency improvements across their

operations. Today, all three are in

short supply.

The development of an end-to-end sustainability production system

will require a systematic approach to the acquisition and development of capabilities

across the workforce. Companies will also

need appropriate supporting infrastructure across the wider organisation. That might include investments in new

analytical tools to help staff interpret sustainability-related data, and

changes to KPIs, targets, and incentives to promote continuous improvements in

energy and resource efficiency.

Several companies are already pursuing this approach. A large-scale, ten-year operational energy-efficiency

programme at one major chemicals player focused on capability building among frontline

process engineers. Hundreds of staff across

the organisation developed the skills to understand the root causes of losses

and process inefficiencies, aided by new analytical tools that helped them

identify and evaluate the impact of detailed process changes.

The programme has reduced carbon emissions by 10% while generating

savings of about €100 million per year. That impact was achieved not through big

investments in new equipment but through dozens of smaller measures scattered across

the business. One site alone implemented more than 30 separate projects. Notably, the company made no special financial

provisions for efficiency improvements; projects had to demonstrate a

three-year payback like any other investment.

The road to net zero involves several distinct steps. Companies must understand their current carbon

footprints, identify strategies to reduce and ultimately eliminate carbon

emissions, and implement the necessary changes.

The drive to reduce Scope 3 emissions generated in the upstream and

downstream value chain, meanwhile, will require companies to extend their sustainability

production systems to include functions such as procurement, product development,

supplier development, sales, and logistics. Measuring, monitoring, and improving Scope 3

emissions in the upstream supply chain will demand extensive changes to current

approaches to supplier selection and management, for example, along with new

analytical skills in the responsible teams. Companies will want a comprehensive carbon

accounting-and-control system that runs alongside its financial equivalent. Such systems are in their infancy today, but

development is accelerating. In

mid-2020, chemicals company BASF began to publish full details of the carbon footprints

of the 45,000 products in its portfolio.

The transition will also require effective cross functional coordination.

Carmakers are already exploring

opportunities to replace high-quality, high-footprint virgin aluminum with

lower-grade, low-footprint recycled aluminum. That calls for collaboration between product

development, sourcing, and manufacturing teams. The ability to demonstrate better

environmental performance can boost sales too. Some materials companies are already using

their sustainability credentials and long-term improvement plans as an argument

for their products over rivals’.

The third critical element required to operationalise a company’s

carbon-reduction strategy is tactical innovation. Many of the moves required to drive down

overall emissions will involve the adoption of new technologies and approaches,

the costs and benefits of which may be highly site-specific. Half of the carbon emitted in ammonia

production is pure CO2, for example — and therefore could be ideal for carbon

capture and storage (CCS). In Europe, ammonia

plants located close to ports have opportunities to transport this gas in

marine tankers for storage in depleted offshore oil and gas wells. Our calculations suggest that this approach

was cash-flow-positive even at the February 2021 carbon price of €40 per ton.

Similarly, advanced heat recovery, zero-carbon electricity,

hydrogen, biomass, and geothermal and nuclear heat are all potential

substitutes for the fossil fuels used to produce process steam. The best choice for a given site will depend

on the local price, societal acceptance and availability of each fuel type.

Companies will need the ability to pilot and scale up new and

unproven technologies within their existing production networks. That will involve partnerships with start-ups

or research organisations to pursue breakthrough innovations — and it will also

require adequately funded and supported in-house capabilities. Government support for such initiatives is

increasingly available. The EU

Innovation Fund, for example, plans to invest €10 billion on low-carbon innovation

over the next decade, with funding earmarked for small-scale projects alongside

flagship innovation efforts. One

candidate for such tactical innovation might be the development of high-temperature

heat pumps to reduce energy consumption in the food industry’s sterilisation

and cooking processes.

Capex-replacement cycles present another opportunity for site-level

innovations and technology investments. A

steelmaker facing a €500 million investment to replace a coke oven battery, for

example, might consider a switch to more efficient alternative technologies, such

as a jet-process basic oxygen furnace. It

could also choose to invest in electric arc furnace technology, switching the

feedstock to direct reduced iron produced using natural gas with CCS, or using

hydrogen.

Once again, these are decisions that cannot be left to the

boardroom alone. The best answers for

any site will depend on specific factors, including its location, the

availability of low-cost capital or government support, and the strength of the

organisation’s long-term commitment to the technology or market segment.

Proven and emerging technologies and operating approaches, if applied

at scale, will be enough to take energy-intensive companies perhaps 40% of the

way along the emissions-abatement curve. The remainder of the journey will require big

bets and big steps into the unknown. As

they consider those choices, businesses will need to decide the strategic

posture they wish to adopt in the carbon transition. Some organisations will seek to play a leading

role, pioneering the adoption of sustainable technologies and business models. Others will adopt a “last man standing” strategy,

seeking to retain their existing approaches for as long as customers and

regulators permit. Between those

extremes, companies may choose to pursue fast-follower or slow-follower

strategies, holding off on major shifts until approaches have been proven

elsewhere (Exhibit 4).

Based on their strategic postures, companies will want to

reevaluate their existing portfolios, potentially disposing of assets or

exiting certain businesses. In other

areas, they will likely need to place their big bets across one or more of

three key dimensions: geographies, products, and processes.

— New geographies: Locating manufacturing facilities for less

energy-intensive products closer to the point of end use can significantly reduce

carbon emissions generated during transportation. For energy-intensive products, proximity to

new feedstock sources or sources of low-carbon energy can be even more advantageous.

Saudi Arabia, for example, has announced

plans to build a new green hydrogen plant powered by 4 gigawatts of wind and

solar energy. Much of the plant’s annual

hydrogen output will be converted to 1.2 million tons of ammonia and exported

worldwide as a low carbon energy source and chemical feedstock. Australia, which has abundant ore resources

and significant renewable-energy potential, could become an advantageous

location for the production of iron using green hydrogen, for example. The move up the value chain, shifting from an

exporter of ore and coking coal to a producer of iron, would generate new value

for the region. And, by halving the mass

of exported materials, it would have a positive knock-on effect on transport

emissions.

— New products: Organisations may choose to shift into

lower-emissions product and market segments. Manufacturers of cement-based building

components might migrate into engineered timber alternatives. Materials players could invest in novel

chemical-based recycling technologies for plastics. Meat and dairy producers could enter new food

categories derived from plants, cultured meat, or insect-based sources of

protein. That shift is already underway,

with major food companies making large investments in the sector. In 2016, dairy products maker Danone made its

largest acquisition in a decade with its US$12.5 billion purchase of WhiteWave,

owner of the Alpro brand of plant-based foods.

— New processes: In many industries, the known technologies

required to deliver net-zero operations are value destroying, if they exist at all.

To remain viable, therefore, companies

will want to radically reinvent their processes. Heavy industrial sectors face a multiyear

effort. Brazilian metals company

Tecnored is developing a more energy-efficient process for production of pig

iron that uses pellets of powdered ore combined with coal or biomass char as a

reducing agent. It has been operating a development

plant since 2011 and, having proved that its process is cost-competitive with conventional

methods, is now working on a commercial unit with a planned annual capacity of

500,000 tons. In the production of

ethylene, Dow and Shell have announced research into electrically powered

steam-cracking technology. Elsewhere,

laboratory-scale demonstrations have shown that replacing the conventional high-temperature

steam-cracking process with chemical looping–oxidative dehydrogenation could

reduce carbon emissions by almost 90%, cut operating costs, and debottleneck existing

assets.

To succeed in these moves, organisations will want to move more

R&D expenditure into sustainability related topics. They have room to do so. In 2020, global R&D expenditure on

technologies to fight climate change was estimated at around US$80 billion. That is less than 5% of the world’s US$1.7

trillion R&D budget.

The transition to net-zero emissions will have a profound impact on

almost every aspect of business. Success

will require a transformational approach.

For industries that have relied on the same fundamental technologies for

a century or more, the degree of change required in the next three decades may

seem formidable, but it is not without precedent. Neither the internet nor the mobile phone had

achieved large-scale adoption at the beginning of the 1990s.

Such a transformation must begin with a decarbonisation vision,

determining the role the organisation seeks to take through the carbon transition

and beyond, and laying out the scale and scope of the operational changes and

strategic big bets required to reach it.

Achieving that change at the necessary pace to meet global climate

goals will still require companies to juggle thousands of initiatives and

develop entirely new technologies, all in an environment of significant

uncertainty. That will require careful planning,

with development of new decarbonisation “playbooks” that help business prioritise

and sequence their carbon-reduction actions. Whatever their strategy, companies must also

adapt targets, performance metrics, and decision-making processes across the

organisation to ensure that staff at every level are motivated and supported to

achieve emissions goals.

Finally, to successfully operationalise their emissions reduction

efforts, companies will need to develop new capabilities at a transformational

scale. That capability-building effort

needs to be broad, equipping the majority of staff with the skills they need to

understand and act on sustainability related sustainability data. It also needs to be deep; developing a task

force of process optimisation and sustainability specialists that can help site

teams to drive rapid improvement, for example.

For any company with ambitions to remain viable beyond the middle

of this century, the race to net zero emissions is already under way. Yet, the formidable technical and economic

barriers they face has left many organisations stuck in the starting blocks,

paralysed by the abatement curve.

Surmounting those barriers will require a transformation mindset

with two primary elements. Beyond the

boardroom, companies will need to operationalise at scale, capturing short-term

value creation opportunities by equipping their frontline staff with new

skills, new tools, new processes, and new infrastructure. Within the boardroom, meanwhile, leaders will

need to rethink their strategic positioning, adapt their existing portfolios, identify

the growth opportunities emerging from the disruption of decarbonisation, and

place big bets on their long-term futures.